MACRON NAMES EDOUARD PHILIPPE PM, MACRON MEET ANGELA

French President Emmanuel Macron has named center-right Republican Party lawmaker Edouard Philippe as prime minister.

France’s presidential office announced the selection of Philippe on Monday, one day after Macron’s inauguration.

Philippe is 46 years old.

Local media report Philippe knew Macron before becoming a lawmaker and that they share many similarities, such as experience working in the private sector.

Local media report Philippe knew Macron before becoming a lawmaker and that they share many similarities, such as experience working in the private sector.

The two leaders have reportedly agreed there is a need to foster unity across party lines.

Macron is expected to select the rest of his Cabinet from the left and right of the political spectrum. The first cabinet meeting is scheduled for Wednesday.

French President Emmanuel Macron and German Chancellor Angela Merkel have agreed to work together to deepen the integration of the European Union.

Macron met Merkel in the German capital Berlin on Monday. He was on his first foreign visit a day after his inauguration.

At a joint news conference after the meeting, Macron noted that he faces many challenges, and that he must implement the reforms that France needs.

Macron expressed his resolve to address the French people’s dissatisfaction with social disparity that was expressed in the presidential election, and to tackle unemployment.

Merkel said the interests of Germany are closely tied to the interests of France. She said that Germany and Europe will only do well if there is a strong France.

The two leaders leaders agreed to jointly draw up a road map to stabilize the eurozone and strengthen the unity of the EU ahead of Britain’s planned exit from the bloc.

There is growing frustration among people in both France and Germany over the EU and its immigration policies. Media agencies

AN ECONOMIC CHARACTERISATION OF SANITATION: BETWEEN THE STATE’S PRODUCTION AND THE HOUSEHOLD’S DEMAND

|

| CPR is pleased to invite you to a CORP seminar on An Economic Characterisation of Sanitation: Between the State’s Production and the Household’s Demand Chloé Leclère |

| Friday, 19 May 2017, 3:00 to 4:30 p.m. |

| Conference Hall, Centre for Policy Research |

| Image Source |

Adam Smith’s ‘invisible hand’ fails to promote sanitation in India. The private or domestic decisions vis-à-vis sanitation, produce negative externalities at the individual and collective levels, consequently, explaining the need for state intervention. In post-colonial India, sanitation has been a public concern since the 1980’s, but the most significant breach is the Total Sanitation Campaign (TSC) which was launched in 1999. The limited impact of this scheme led to a research agenda to explore the efficiency of the policy by examining factors such as good governance, devolution of funds and participatory development. The literature focuses on supply driven model to ensure provision of sanitation by the state on one hand and on the other hand, it highlights the determinants of the sanitation demand that have gained visibility with community led programs that reject monetary subsidies and focus on awareness and education.

Although economic terms prevail in the media, political and scientific debates, little attention is paid to the nature of sanitation as an economic good. It is yet a fundamental preliminary question that shapes the sanitation outcomes and helps to understand the behavior of all the actors involved. No theoretical framework is immediately adaptable to describe sanitation and its price. In fact, the main vector of information in Economics, is an unknown variable as there is no proper market. Based on the review of literature and close examination of several datasets [India Human Development Survey (IHDS), Census, National family Health Survey-III (NFHS-III), Sanitation Quality, Use, Access and Trends (SQUAT) survey], three major characteristics of sanitation in India have been identified. This talk will explore questions pertaining to the need of sanitation, what it produces and the process that relates a biologic imperative and the environment circumscribe a multi-dimensional scape.

Chloé Leclère is a PhD Scholar in Economics at the Ecole Normale Superieure de Lyon in France. Her research focuses on sanitation policies in India and explores the specificities related to evaluation of social programmes. She is a member of the research laboratory- Groupe d’Analyse et Théorie Economique Lyon-Saint Etienne in France. She is also affiliated with the Center for Social and Human sciences (CNRS, Ministry of Foreign Affairs) in New Delhi where she is conducting several projects on poverty alleviation in India. She is a former Teaching Fellow at the ENS de Lyon. She holds a Master’s degree in Economic Analysis and Policies from Paris School of Economics in France and another Master’s in Social Sciences from Ecole Normale Supérieure de Lyon in France.

Please RSVP to sci-fi@cprindia.org

CORP Seminar Series

This is the 12th in the series of the Community of Research and Practice (CORP) seminar planned by the Scaling City Institutions for India: Sanitation (SCI-FI: Sanitation) initiative. This seminar series aims to provide a platform for discussing the experiences of the researchers and practitioners on urban sanitation. Through these discussions, the sanitation initiative intends to build a stronger evidence base for developing policies, programmes and implementation of plans for achieving sanitised cities. |

PROMOTION OF COMEDY FILM ‘JATTU ENGINEER” IN DELHI

Saint Gurmeet Ram Rahim Singh Insan promoted his upcoming comedy film ‘Jattu Engineer” in Delhi

Dr.MSG aka Saint Gurmeet Ram Rahim Singh Insan promoted his upcoming comedy flick “Jattu Engineer” out here in Nation’s Capital Delhi. After box office success of Hind Ka Napak Ko Jawab, Dr.MSG is all set to hit the big screen again with “Jattu Engineer”.

This is going to be his first comedy film. And just like four previous action movies of MSG-series, the father-daughter duo, Saint Dr.MSG and his daughter Honeypreet Insan has directed this movie. “Jattu Engineer” will be a comedy movie with some social messages knitted in humour and emotions. The storyline revolves around an underdeveloped village that is struck by poverty, unemployment, and drug menace and how a teacher transforms the fate of the villagers with his deep-dyed gumption to uplift the living standards of the village. The movie will also highlight the PM Narendra Modi’s dream project – Swachh Bharat Mission.

Well, while asking him about the Delhi Cleanliness Mission, Saint Gurmeet stated, “This time it didn’t took much time to clean Delhi, in comparison with last 2 times, which is good for the Capital. It proves that Delhi is following the cleanliness mission.”

The shooting of “Jattu Engineer” was completed in a short span of 15 days. The music of the movie is composed by Gurmeet Ram Rahim Singh himself. Featured by Hakikat Entertainment Pvt.Ltd. “Jattu Engineer” is slated to release on coming 19th of May.

NIDDHI AGERWAL ON A HOUSE HUNT !

After a nationwide talent hunt , director Sabbir Khan finally found his leading lady for his next film , Munna Michael, starring Tiger Shroff.

Niddhi who is a professional ballet dancer , happened to be selected quite by accident but was immediately signed thanks to her screen presence and charisma, not to mention her acting talent and dancing skills.

The debutante may have received a warm welcome from the film industry but unfortunately was forced to move out of her flat in the suburbs , as the housing society raised objections to her ‘single actress’ status.

Sources reveal that society boards are generally wary of letting out flats to aspiring actors , leaving Niddhi no choice but to hunt for a new apartment.

She says, “I have lived with my friend for nearly six months. Now, hunting for a new place seems an impossible task.Because I am single and an actress, I have been denied accommodation. As of now, that’s the biggest hurdle that I have faced here.”

MAN TRUCKS DELIVERS NEW CLA EVO VEHICLES TO CUSTOMERS

MAN Trucks delivers New CLA EVO vehicles to customers

Company crosses important milestone with roll out of

25,001st truck from Pithampur facility

25,001st truck from Pithampur facility

Indore.16th May, 2017: MAN Trucks India, 100% subsidiary of MAN Truck & Bus AG, Germany, rolled out the New CLA EVO range. The initial trucks were delivered to customers recently at an event at the company’s facility at Pithampur, Indore. In the process, MAN Trucks also crossed an important milestone in its India journey – over 25,000 vehicles sold in India as well as in export markets. The new range was unveiled at the BAUMA CONEXPO INDIA in December 2016.

The market introduction of the new range also coincides with the BSIV emission norms that came into effect on 1st April, 2017. The series includes tippers, rigids and tractors, besides special application trucks that address diverse customer requirements. These are designed to operate in tough operating conditions with high performance and efficiency levels.

Mr. Joerg Mommertz, Chairman and Managing Director, MAN Trucks India said, “At MAN, it is our endeavour to provide best-in-class solutions for the transport and infrastructure sectors. We have always listened to our customers to understand their changing requirements. The new CLA EVO range is a good example of our ability to develop solutions in India, for India. MAN trucks are seen as a reference for strong performance over long duty cycles. Going forward, we will work towards bringing newer solutions to raise the bar for our customers.“

With new benchmarks, the CLA EVO series offers a combination of power, fuel efficiency, world class performance and safety. The trucks are powered by the proven MAN D-0836 common rail engine that delivers 250HP and 300HP based on the application. At the same time it complies with the BSIV emission norms.

Coupled with a well configured driveline, the engine delivers best-in-class fuel efficiency. Extensively tested to global standards and equipped with strong aggregates and a robust chassis frame and suspension, the CLA EVO range meets the highest operating standards under extreme conditions.

“With the implementation of GST, demand for haulage trucks is expected to rise. The MAN long haul trucks can operate up to 20 hours duty cycles, which will benefit operators in terms of faster turnaround. The engines have been been enhanced to deliver more power, while being fuel efficient. Besides the product range, we are also expanding our after sales service network in order to cater to requirements across all key routes and locations,“ Mr. Mommertz added.

Presenting the New MAN CLA EVO range

The New CLA EVO series comprises tippers, long haul and special application trucks ranging from 16T to 49T.

The trucks are powered by the proven MAN D-0836, turbo charged, inter-cooled engine, that are rated for 250HP and 300HP. Mated with 6- and 9-speed gearboxes, the trucks are adapted for specific operational purposes. The electronically controlled Common Rail system makes the engine reliable and fuel efficient than before, besides being environment friendly.

The crawler gear in long haul trucks helps the engine run within the optimal rpm range, thereby reducing fuel consumption.Strong rigid front axle, hypoid rear axles provide superior traction&gradeability, and unmatched reliability.

The tippers feature MAN‘s planetary rear axle with hub reduction, which provides high ground clearance and has proven its effectiveness in varying conditions. The inter axle and differential lock imparts superior traction.

The driver environment offers best-in-class ergonomics, visibility and control. The objective is to provide drivers high levels of comfort for significantly reduced fatigue and enhanced safety. The aerodynamic cabin with heat and sound dampeners, and an optional AC helps maximise man and machine performance and productivity. The driver cabs also offer sleeper berths in the long haul trucks.

MAN Aftersales and Service

MAN Trucks India offers service and support to ensure maximum uptime, all the time. MAN Services offers include warranty schemes, annual maintenance contracts, on-site support and 24×7 helpline service.

MAN Services also offer new solutions like lubricants that can improve the engine performance. Along with MAN genuine parts, always recommended to operators, the vehicle life cycle gets a boost – whether it is in engine hours for tippers or kilometres clocked for long haul trucks.

About MAN Trucks India

MAN Trucks India Pvt. Ltd. is a fully owned subsidiary of MAN Truck & Bus AG, Germany. The company has its Head Quarters in Pune and state-of-the-art manufacturing facility at Pithampur, Madhya Pradesh. The product range manufactured in this plant include tippers for off-road& construction, haulage for regular & over dimensional cargo, and special application trucks such as fire tenders, garbage compactors, concrete mixers, boom pumps, tip trailers and bulkers. The product range for India is developed at MAN Trucks R&D centre in Pune. The trucks made in India are also exported to African and Asian markets. MAN Trucks offers prompt and efficient support through its network of 63 touch points in India and one each in Bangladesh, Bhutan and Nepal. The company has sold over 25,000 trucks since it started its India operations in 2006.

MAN TRUCKS INDIA PVT.LTD.

Pride Silicon Plaza

Senapati Bapat Road

Pune 411016

PRESS ADVISORY

PRESS ADVISORY

(1) Press Conference (Through Video Conference)

Sh. Piyush Goyal, Minister of State (I/C) for Power, Coal & renewable Energy will be addressing press conference on Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY) Rural Electrification Programme and to highlight achievements of the Government, at 11 am to 1.30 PM on Friday , 19th May 2017.

Date : 19-05-2017, Friday

Time : 11:00 AM

Venue : NIC conference room, Collector office,

Ground Floor, Ahmedabad.

(2) Press Conference (Through Video Conference)

Union Minister for Science & Technology and Earth Sciences, Dr. Harsh Vardhan will address the press conference on achievement of 3 years on the 19th May, 2017.

Date : 19-05-2017, Friday

Time : 03:00 PM

Venue : NIC conference room, Collector office,

Ground Floor, Ahmedabad.

Separate registration for both conferences is required.

Maximum 10 journalists can be accommodated in NIC conference room.

Registration can be done on whatsapp/Call 9429029268,

Email pibahmedabad1964@gmail.com and Phone no. 079-25507041.

‘CREATING AN ENABLING ENVIRONMENT FOR RETURNEE ENTREPRENEURS’

Dr A Didar Singh

Secretary General

May 16, 2017

Mr N.K. Sagar

Editor Topix, Europe, Germany-New Delhi

Enkay Sagar Holdings Pvt. Ltd.

New Delhi

Dear Mr Sagar,

The Federation of Indian Chambers of Commerce and Industry (FICCI) has the pleasure of inviting you to participate in a consultation on ‘Creating an Enabling Environment for Returnee Entrepreneurs’ on July 27th, 2017 at Federation House, Tansen Marg, New Delhi at 9:30 am.

The idea that migration of skilled individuals from developing to developed countries leads to a ‘brain drain’ has come to be replaced by the concepts of ‘brain circulation’ and ‘brain gain’ – which occurs when talented people return with newly absorbed technologies, networks, technical expertise, managerial skills and the like. Perhaps owing to these risk taking abilities illustrated by their decision to move in the first place, migrants often return to their country of origin to start their own businesses. The entrepreneurial process on their return is accompanied by several challenges which tend to be unique and different from those faced by local entrepreneurs, even though there are overlaps.

The consultation is aimed at bringing together all relevant stakeholders to discuss the findings of a research project being undertaken FICCI, in partnership with the Hong Kong University of Science and Technology, on the return migration of entrepreneurs to India in light of the Chinese experience. The conference will also serve as a platform for discussing and throwing light on issues faced by returnee entrepreneurs in India, and deliberating on solutions, including the possibility of putting in place an institutional mechanism for providing support to the Indian diaspora wishing to return and start enterprises back home

Please find enclosed a copy of the draft programme for your reference.

We hope that you will be able to join us for this significant event. Please RSVP by sending an e-mail to kanika.malik@ficci.com

I look forward to hear from you.

With Best Regards,

Yours Sincerely,

(A Didar Singh)

‘MEGA COW MILK PARTY TO PROTECT COW SLAUGHTER

PRESS INVITATION

Hakikat Entertainment Pvt.Ltd. cordially invites you on ‘Mega Cow Milk Party to protect Cow Slaughter’ at Premiere of

‘Jattu Engineer’

(Where Saint Gurmeet Ram Rahim Singh Insan will give a “Cow Milk Party” to 20,000 people present at the event and appeal Prime Minister Narendra Modi to make Cow the National Mother of India)

This will be followed by a pledge, to be taken by 20,000 people present at the event to PROTECT COWS FROM KILLING.

Time: 12noon

Date: 17th May 2017, (Wednesday)

Venue: Indira Gandhi Indoor Stadium, ITO

WORLD ECONOMIC SITUATION AND PROSPECTS: MAY 2017 BRIEFING, NO. 102

WORLD ECONOMIC SITUATION AND PROSPECTS: MAY 2017 BRIEFING, NO. 102

- Slowdown in productivity growth posing a medium term challenge for developing countries

- Weaker-than-expected first quarter growth in the United States of America

- Plunge in cocoa prices delaying economic recovery in West Africa

GLOBAL ISSUES

RECENT SLOWDOWN IN PRODUCTIVITY GROWTH HIGHLIGHTS MEDIUM-TERM CHALLENGES FOR DEVELOPING COUNTRIES

Recent indicators have shown a gradual strengthening of global economic activity since late 2016. In tandem with an improvement in aggregate demand, international trade and manufacturing output have rebounded, while commodity prices have risen from their lows seen in early 2016. Amid a general improvement in business sentiment, several large economies, including the United States of America and Japan, are experiencing a moderate recovery in investment. Against a backdrop of elevated uncertainty and downside risks, however, it is still unclear whether this positive global growth momentum can be sustained going forward. Several lingering structural weaknesses are also constraining the medium-term growth outlook. Of particular concern is the prolonged and broad-based weakness in global productivity growth since the global financial crisis.

Figure 1 compares labour productivity growth trends in developed and developing regions between 1995 and 2016. Prior to the 2008-09 crisis, developing economies had been experiencing a rapid acceleration in labour productivity growth. In contrast, average productivity growth in developed countries had been on a longer term downward trend. In recent years, while productivity growth in developing economies has been steadfast than in developed countries, its pace has slowed considerably compared to the pre-crisis period. This persistent weakness in productivity growth has generated widespread concern given that it is a long-term determinant of income and living standards. For developing economies, prolonged weak productivity growth will not only adversely impact medium-term growth prospects, but may also severely undermine progress in achieving the Sustainable Development Goals. It is therefore important for policymakers to understand the factors driving slower labour productivity growth in developing economies.

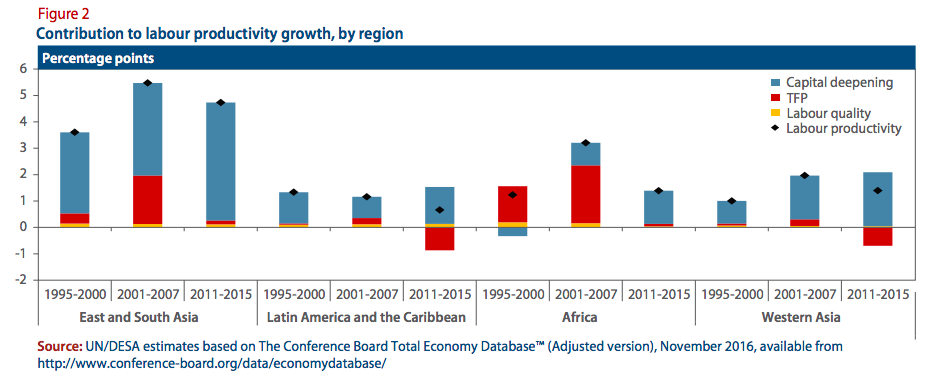

Labour productivity is commonly measured as total output per person employed, or as total output per hour worked. Growth in labour productivity for an economy is driven by three key factors, namely, improvements to labour quality; capital deepening (available capital per worker); and, growth in total factor productivity (TFP). TFP is a measure of an economy’s efficiency in allocating its factors of production and is influenced by various factors, including economies, the slowdown in labour productivity growth has been largely attributed to the decline in the contribution from capital formation. This reflects the persistent weakness in investment growth in these economies since the financial crisis, as capital spending remains constrained by sluggish demand, high uncertainty and fragile bank balance sheets.

Across many developing regions, however, capital deepening has continued to contribute positively to labour productivity growth, implying that investment in new capital has held up relatively well in the post-crisis period (figure 2). Instead, the recent slowdown in labour productivity growth in developing countries has been mainly due to a deceleration in TFP growth. is suggests that developing countries are, on average, experiencing slower efficiency gains and technological absorption following the recession.

Several cyclical and structural factors appear to have contributed to the broad-based slowdown of TFP growth in developing economies. On the cyclical front, subdued demand conditions—amid high uncertainty in the post-crisis environment—may have affected the quality of investment, resulting in lower TFP growth. In addition, recent evidence has shown that TFP growth in the commodity-exporting economies tends to move in tandem with commodity prices, given that commodity-related income facilitates investment in technology and human capital. Hence, the end of the super-cycle of commodity prices in recent years has contributed to the slowdown in productivity growth in several regions, including in Africa, Latin America and Western Asia.

Beyond these cyclical factors, several structural shifts had also taken place, notably the waning effects of past advances that catalysed strong TFP growth in the last two decades. First, the surge of information and communication technology in the 1990s contributed to improved productivity in the global economy, including in developing economies. Second, earlier structural reforms and transformation processes spurred large productivity gains in several countries. For instance, China’s transition from an agrarian economy to an industrial powerhouse was accompanied by rapid technological progress and increased workforce efficiency. Third, major trade liberalization efforts, such as the formation of the European Union and China’s accession into the World Trade Organization, drove rapid growth in international trade in the 2000s. This development could have stimulated TFP growth in many developing economies, given that trade increases competition and drives the distribution of new technology. In particular, the proliferation of global value chains, for example in East Asia, not only generated large economies of scale, but also allowed for exporting firms to acquire new production techniques.

It is also important to highlight that a country’s potential to achieve stronger productivity growth is also influenced by its economic structure. Countries with a high dependency on natural resources face larger constraints to productivity growth, compared to countries where high technology manufacturing activities are more prevalent. In general, developing regions like Latin America or Western Asia have had limited success in promoting a process of structural change towards more technologically advanced sectors, thus restraining productivity gains through technical progress and innovation.

In the medium term, policy efforts in developing countries need to be geared towards reversing the current trends in productivity growth to enhance economic resilience and sustain growth prospects. Further progress needs to be made on structural reforms that can boost TFP growth. This includes strengthening governance, improving the quality of education and promoting initiatives to enhance innovation as well as investment in research and development.

DEVELOPED ECONOMIES

UNITED STATES: DISAPPOINTING START TO 2017

Gross domestic product (GDP) growth in the United States was on the downside in the first quarter of 2017, with the advance estimate showing growth of just 0.7 per cent on an annualized basis. While consumer confidence indicators rose following the elections in November 2016 and remain high today, this has not yet translated into stronger household spending. Personal consumption expenditure showed negligible growth in the first quarter of the year, with a sharp decline in spending on durable goods. A downward adjustment to the level of private inventories also contributed to the economic slowdown, reducing GDP growth by 0.9 percentage points. There is a risk that the weaker-than-expected GDP growth may lead to a reversal of the upbeat economic sentiment and buoyant stock market performance in the United States, putting the Government’s target of achieving annual GDP growth of 3 to 4 per cent further from reach.

The Federal Open Market Committee (FOMC) of the United States Federal Reserve kept interest rates unchanged at its meeting in May. While financial markets continue to expect a 25 basis points rise in interest rates in the United States at the next monetary policy meeting in June, the FOMC may move more slowly if confidence indicators deteriorate or if signs of an acceleration in real economic activity fail to emerge.

JAPAN: UNEMPLOYMENT RATE AT 22-YEAR LOW

The unemployment rate in Japan dropped to 2.8 per cent in February and remained stable in March, the lowest level recorded since 1994. At the same time, the Tankan factor utilization index stands at its highest level since 1990 and the Bank of Japan’s (BoJ) estimate of the output gap is positive, showing positive gaps in both labour and capital inputs. The BoJ is committed to maintaining its policy of “Quantitative and Qualitative Monetary Easing with Yield Curve Control”, aiming to achieve the price stability target of 2 per cent. Nonetheless, wage pressures remain moderate and inflation is unlikely to reach the central bank target this year or next. Nationwide consumer price inflation averaged -0.1 per cent in 2016, but has been positive in the first months of 2017, hovering close to zero. The uptick in inflation, which reached 0.2 per cent in March, primarily reflects higher energy prices and the depreciation of the yen in late 2016.

EUROPE: SLOWER INFLATION AND SOLID GAINS IN NOMINAL WAGES

In March, inflation in the European Union slowed to 1.6 per cent from 2.0 per cent in the previous month, due mainly to a slower increase in energy prices. Romania, with 0.4 per cent, and Ireland and the Netherlands, both with 0.6 per cent, registered the lowest inflation rates in the region, while Latvia and Lithuania experienced the fastest price increases, at 3.3 per cent and 3.2 per cent, respectively. At the same time, nominal wages showed solid gains in several countries. In Germany, nominal wage growth in industry reached 3.0 per cent in February, which translated into some gains in real purchasing power due to the moderate level of inflation. Similarly, in Poland, the average wage level increased by 5.2 per cent in March, although one o payments underpinned part of this increase. In both cases, these trends will further drive private consumption, which has been playing an important role for the overall growth performance.

As inflation in the Czech Republic was unexpectedly on the upside in March, reaching 2.6 per cent, in early April the Czech National Bank concluded its policy of maintaining a ceiling on the value of the koruna, which was initiated in late 2013 as an additional monetary policy tool.

ECONOMIES IN TRANSITION

In the first quarter, macroeconomic indicators in the Commonwealth of Independent States (CIS) area show a heterogeneous growth performance. In Central Asia, Kyrgyzstan recorded strong GDP growth of 7.8 per cent as gold production increased, while a recovery in remittances from the Russian Federation bolstered household income. In the Caucasus, the economic activity indicator strengthened by 6.6 per cent in Armenia. Among the CIS energy-exporters, the implementation of development programmes contributed to 3 per cent growth in Kazakhstan. In contrast, the Azerbaijan economy shrunk by 0.9 per cent, largely due to a drastic decline in oil output. This was attributed in part to the commitment to production cuts as agreed by Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC members at the end of 2016.

Inflationary trends in the region also diverged. Armenia saw a 0.9 per cent deflation in the first quarter. In Azerbaijan, however, inflation accelerated to 14.5 per cent in March, driven by higher food prices. Inflation also increased in Ukraine to 15.1 per cent, due to higher production costs.

In the Russian Federation, inflation is contained at slightly over 4 per cent, in part held back by subdued domestic demand, but also the strong rouble bringing down import prices and inflationary expectations. In late April, the central bank further reduced its policy rate by 50 basis points to 9.25 per cent. Due to still high real interest rate, however, this move will impact carry trade and the exchange rate only moderately. Policy rates were also reduced in Belarus, where inflation subsided considerably alongside an appreciation of the domestic currency, and in Ukraine.

In South-Eastern Europe, the Albanian economy expanded by over 3.4 per cent in 2016. Robust export performance significantly contributed to growth in the fourth quarter. The country has absorbed about €1 billion of foreign investments in 2016.

DEVELOPING ECONOMIES

AFRICA: PLUMMETING COCOA PRICES HIT WEST AFRICAN ECONOMIES

Plummeting prices are hurting the finances of cocoa producing countries and incomes for hundreds of thousands of small-scale farmers. Cocoa prices have plunged by over 40 per cent since last year, hitting a 10-year low, as a result of bumper crops and stagnant demand around the world. Cocoa is the main produce of Côte d’Ivoire and accounts for about a fifth of the nation’s exports. It is also among the main exports of Cameroon, Ghana, Guinea, Nigeria, São Tomé e Príncipe and Sierra Leone.

In Cameroon, the price decline is affecting 600,000 households whose livelihoods are derived from cocoa. Ghana, the second largest world producer of cocoa, has lost almost $1 billion in export revenue. Côte d’Ivoire, the world’s top cocoa exporter, announced that it would reduce its 2017 budget by one tenth, although the move was also triggered by wage demands from civil servants and soldiers. The decision follows a recent one to cut prices paid to farmers by 36 per cent, as a disincentive to raise output. In the coming months, the World Bank will grant the country $100 million to $125 million in budget support. Cocoa-growing countries plan to fight the price rout by coordinating production strategies and promoting local consumption of chocolate.

There is, however, room for some optimism. Though a production surplus is likely to last through this year, the price weakness is not uncharacteristic of the market, which has seen considerable historical volatility. Most importantly, there is potential for growth in world cocoa consumption, given the possible demand growth in developing markets over the long term.

EAST ASIA: FIRST QUARTER GROWTH EXCEEDS EXPECTATIONS

Amid an improvement in domestic demand and a recovery in exports, a few major East Asian countries experienced faster-than-expected growth in the first quarter of 2017. In China, GDP growth picked up slightly to 6.9 per cent on a year-on-year basis. The industrial sector expanded at a stronger pace, driven in part by government stimulus measures and continued rapid credit growth. In the tertiary sector, services such as accommodation, real estate, retail and finance grew at a faster pace. However, these improvements were more than offset by a deceleration in transport and other services. From a demand perspective, private consumption remained the largest contributor to GDP growth, supported by a rise in disposable income and stronger job creation. Growth in fixed asset investment also accelerated, driven mainly by infrastructure and real estate investment.

Despite high political uncertainty, the economy of the Republic of Korea expanded at a faster pace of 2.7 per cent in the first quarter. Exports rebounded during the quarter, bolstered by an increase in shipments of semiconductors and machinery and equipment. Growth was also supported by stronger investment in facilities and sustained private consumption. Similarly, Taiwan Province of China also grew at a faster-than-expected pace of 2.6 per cent, driven mainly by higher exports of electronics. In addition, the recent announcement of a $29 billion (5.2 per cent of GDP) stimulus package, spread over 8 years, will provide a boost to domestic demand going forward.

SOUTH ASIA: PAKISTAN’S EXTERNAL SECTOR DETERIORATES VISIBLY, UNDERSCORING MEDIUM-TERM CHALLENGES

Since early 2016, the external sector has visibly deteriorated in Pakistan, owing to largely stagnant exports and a significant rise in imports. In the nine months to March 2017, the trade deficit increased by 28 per cent year-on-year to a record high of $19.7 billion, with the monthly import bill surpassing $5.0 billion for the first time in March. In particular, export growth has been restrained by relatively subdued external demand, growing competition in the garment sector from other Asian economies, and structural constraints, including power shortages. Meanwhile, imports of goods have increased markedly due to the implementation of large infrastructure projects, including the Pakistan-China Economic Corridor. As a result, the current account deficit has widened considerably, while international reserves declined from almost $19 billion in October 2016 to $17.1 billion in February 2017. These developments have prompted the Government of Pakistan to seek additional foreign loans from multilateral institutions and Chinese State-owned banks. In the short-term, the Pakistan economy is expected to navigate these external headwinds, amid solid private consumption and investment demand. In the medium term, however, strengthening the competitiveness of exports in Pakistan is a key challenge in order to reduce its external fragilities and to achieve a stronger, more balanced and sustainable growth.

WESTERN ASIA: RISING UNEMPLOYMENT

Unemployment rates are climbing in Western Asia, except for Israel where the unemployment rate remains at a historically low level. The Turkish unemployment rate reached 13 per cent in January 2017, the highest since February 2010. The unemployment rate among the Saudi nationals, excluding foreign labour, stood at 12.3 per cent in the fourth quarter of 2016, the highest since the first half of 2012. The unemployment rate of Jordan remained at 15.8 per cent in the fourth quarter of 2016, the highest since 2003. The large number of settled Syrian refugees and evacuees has pushed up the unemployment rate in Jordan and Turkey, where employment creation has also been held back by stagnated growth. For Saudi Arabia, a surge in the female unemployment rate is a dominant factor behind rising unemployment. While the male Saudi unemployment rate stood at 5.3 per cent in the fourth quarter of 2016, the female Saudi unemployment rate stood at 34.5 per cent. This partly reflects the rising female labour participation rate in recent years, from 12.6 per cent in 2006 to 19.3 per cent in the fourth quarter of 2016.

LATIN AMERICA AND THE CARIBBEAN: PROLONGED ECONOMIC CONTRACTION HAS ADVERSELY IMPACTED THE REGION’S LABOUR MARKET

Two years of economic contraction in Latin America and the Caribbean have had a pronounced impact on the region’s labour market. The average urban employment rate has declined steadily since early 2014 as economic activity in South America weakened substantially. At the same time, the quality of employment, as measured for example by the share of vulnerable employment, has worsened. Average unemployment in the region is estimated to have risen from 7 per cent in 2014 to 9 per cent in 2016 with a further increase projected for 2017. Brazil’s labour market has been hit particularly hard, with unemployment rising from a low of 6.2 per cent in late 2013 to 13.2 per cent by February 2017. In parallel, Brazil’s employment-to-population ratio has fallen to the lowest level since the series began in 2012. Most other South American economies have also seen unemployment increase over the past two years, albeit at a much lower rate. Recent labour market trends in Mexico and Central America have generally been more favourable although the subregion continues to face significant structural problems. Mexico’s unemployment rate fell to 3.2 per cent in March 2017, the lowest level in almost a decade. The incidence of informal work has also declined, but remains high at 57 per cent of total employment.

No comments:

Post a Comment